Example of Our AI Blogging Engine.

The content, images, infographics & SEO were all created by our AI system.

Does Commercial Property Insurance Cover Flood Damage

Water damage can wreak havoc on commercial properties, leading to costly repairs and business disruptions. At Tosten Marketing, we often hear from business owners wondering about their insurance coverage for such incidents.

Commercial property insurance water damage coverage is a complex topic with many nuances. This blog post will explore what types of water damage are typically covered, common exclusions, and additional coverage options to consider for comprehensive protection.

What Water Damage Does Commercial Property Insurance Cover?

Commercial property insurance covers several types of water damage, but understanding the specifics is vital. Many business owners find themselves surprised by what their policies do and don’t cover.

Sudden and Accidental Water Damage

Most commercial property insurance policies cover sudden and accidental water damage. This includes events like:

- Unexpected pipe bursts

- Malfunctioning appliances causing floods

For instance, if a washing machine in your commercial laundromat breaks and floods the premises, your policy will likely cover the damage.

Storm-Related Water Damage

Water damage from storms often receives coverage, but with certain conditions. If rain enters through a roof damaged by wind or hail, the resulting water damage typically falls under the policy. However, if poor maintenance caused the roof’s condition, your insurer might deny the claim.

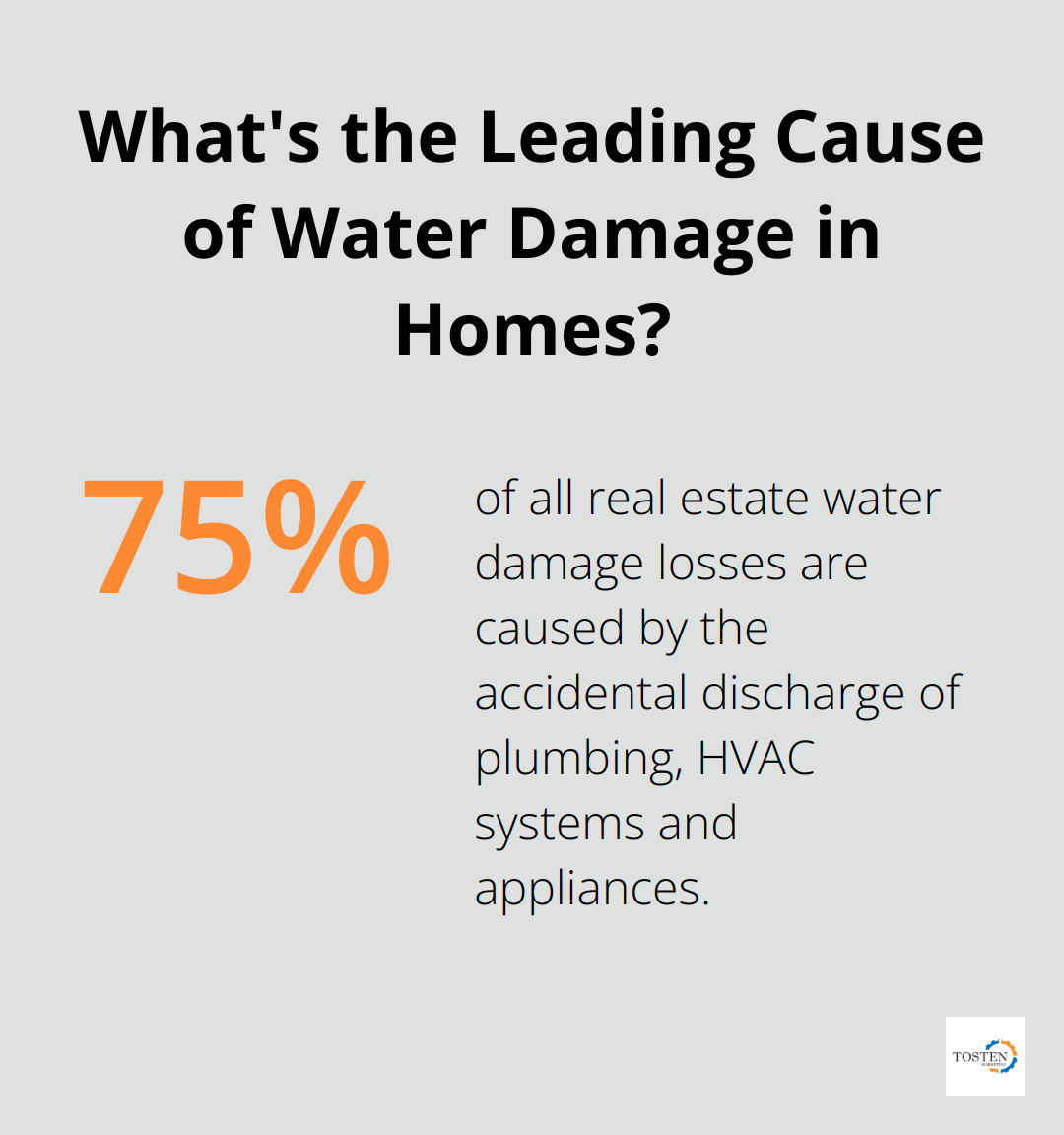

About 75% of all real estate water damage losses are caused by the accidental discharge of plumbing, HVAC systems and appliances.

Sprinkler System Malfunctions

Damage caused by faulty sprinkler systems usually receives coverage under commercial property insurance. This proves particularly important for businesses with extensive sprinkler systems for fire protection. If a sprinkler head malfunctions and soaks inventory or equipment, your policy should cover the losses.

Policy Variations and Quick Action

While these types of water damage generally receive coverage, specifics can vary significantly between policies. We recommend a thorough review of your policy (or consultation with an insurance professional) to understand your exact coverage.

Quick action when water damage occurs can mitigate costs and prevent severe issues like mold growth (which may require costly remediation). Data from Chubb shows that the average loss from a commercial water damage claim reached approximately $89,000 in 2019.

Preventive Measures

To protect your business further, implement preventive measures such as:

- Regular maintenance checks of plumbing and appliances

- Installation of water detection systems

- Conducting regular plumbing inspections

Some insurers may even offer premium discounts for businesses that take these proactive steps.

While understanding what your policy covers proves essential, knowing what it doesn’t cover holds equal importance. Let’s explore some common exclusions in commercial property insurance for water damage.

What Water Damage Isn’t Covered?

Commercial property insurance doesn’t cover all types of water damage. Business owners must understand these exclusions to avoid unexpected costs and ensure proper protection.

Gradual Water Damage

Most policies don’t cover damage that occurs slowly over time. This includes:

- Leaky pipes that drip for months

- Ongoing seepage through foundation cracks

- Mold growth from persistent moisture issues

These issues often result from poor maintenance. Insurance companies expect property owners to address these problems promptly. Regular inspections and swift repairs are essential to prevent gradual damage and maintain coverage eligibility.

Natural Disaster Flooding

Standard commercial property policies typically exclude flooding caused by natural disasters. This includes:

- Storm surges

- River overflows

- Heavy rainfall leading to ground saturation and flooding

The National Flood Insurance Program (NFIP) reports that just one inch of floodwater can cause up to $25,000 in damage. Businesses in flood-prone areas should consider separate flood insurance policies to fill this coverage gap.

Sewer and Drain Backups

Many policies exclude damage from sewer backups or overflowing drains. This type of water damage can be particularly costly and unsanitary. The average flood insurance policy costs $540 a year, according to the NFIP.

To protect against this risk, businesses can often add sewer and drain backup coverage as an endorsement to their existing policy. This additional coverage is particularly important for businesses with basement spaces (or those in areas with aging infrastructure).

Ground Water Seepage

Water that seeps through basement walls or foundations is typically excluded from coverage. This type of damage is often considered a maintenance issue rather than a sudden, accidental event.

Businesses can mitigate this risk by:

- Installing proper drainage systems

- Maintaining gutters and downspouts

- Applying waterproof sealants to basement walls

Understanding these exclusions emphasizes the importance of comprehensive risk management. While insurance is a key component of protection, proactive maintenance and targeted coverage additions play vital roles in safeguarding your business against water damage.

To ensure full protection against water-related risks, businesses should explore additional coverage options that complement their standard commercial property insurance. Let’s examine some of these crucial supplementary policies in the next section.

Why Additional Coverage Is Essential

Flood Insurance: A Critical Safeguard

Standard policies typically don’t cover flooding. Floods can happen anywhere – just one inch of floodwater can cause up to $25,000 in damage. Most homeowners insurance does not cover flood damage. Businesses in flood-prone areas need separate flood insurance. This coverage protects against damage from rain or flash floods, events that occur more frequently due to climate change.

Sewer and Drain Backup: An Often Overlooked Risk

Sewer backups cause extensive damage and pose health hazards. Many business owners don’t realize their standard policy excludes this. Adding sewer and drain backup coverage as an endorsement protects businesses, especially those with basement spaces or in areas with aging infrastructure. The cost of this additional coverage is often minimal compared to potential losses from a single incident.

Business Interruption Insurance: Protecting Your Bottom Line

Water damage often forces businesses to close temporarily for repairs. Business interruption insurance covers lost income and ongoing expenses during these periods. The Federal Emergency Management Agency states that 40% of businesses never reopen after a disaster. This coverage can determine whether a business recovers or closes permanently.

Equipment Breakdown Coverage: Safeguarding Your Assets

Water damage destroys expensive equipment. Equipment breakdown coverage protects against losses from electrical or mechanical failures (often excluded from standard policies). This proves particularly important for businesses that rely on specialized machinery or technology.

Investing in these additional coverage options might seem expensive, but the potential return on investment is substantial. A comprehensive insurance strategy tailored to specific risks can save a business from financial ruin when unexpected water damage events occur.

Final Thoughts

Commercial property insurance water damage coverage requires careful consideration. Standard policies cover sudden and accidental water damage, but often exclude gradual damage, flooding from natural disasters, and sewer backups. Business owners must review their policy details thoroughly and regularly to ensure adequate protection as risks evolve and businesses grow.

Insurance professionals can help navigate the intricacies of commercial property insurance (identifying potential gaps in coverage and recommending additional policies or endorsements). They provide expertise in understanding fine print and ensuring clients aren’t caught off guard by exclusions or limitations. Supplementing standard commercial property insurance with flood insurance, sewer and drain backup coverage, and business interruption insurance creates a comprehensive protection strategy.

Tosten Marketing understands the importance of protecting business assets. We specialize in protecting businesses in Washington State and recognize the value of comprehensive insurance coverage for all businesses. Our expertise in the commercial insurance industry allows us to create comprehensive business insurance solutions that protect our clients.